|

Casualty insurance coverage is a kind of insurance that covers you if you're lawfully accountable for another person's injuries or home damage, such as from a car mishap or an accident in your home. Listed below, we take an in-depth take a look at what casualty insurance coverage is, how it works, who files the claim, and whether it's worth getting or increasing your protection. Casualty insurance safeguards you when you're liable for somebody getting hurt or their belongings getting damaged. The scenarios in which you're covered depend upon the specifics of your policy. For instance, an automobile insurance plan might pay to fix a next-door neighbor's fence after you drove into it. Casualty insurance coverage doesn't cover your own injuries or residential or commercial property damage, or those of other individuals noted in your policy. If you own a business, business casualty insurance can safeguard you when a customer is hurt by among your items or services. Casualty insurance coverage is normally bundled into your insurance coverage policy, so you spend for it when your insurance expense is due. Your policy and quotes might define just how much you pay for each protection, making it simpler to change limitations to fit your spending plan and requirements. When looking at your policy, you'll generally discover casualty insurance under protections for others when you're at fault. There are numerous scenarios where your casualty insurance would start to cover costs. For instance, house insurance may pay for expenditures and legal fees related to:: A visitor trips on their feet while in your house and breaks a wrist.: Your canine breaks free throughout your early morning walk and bites another dog.: A windy day triggers a branch from a tree on your residential or commercial property to break and put a hole in the neighbor's roof. Car casualty insurance can enter into play in a variety of circumstances, such as when someone in another cars and truck is injured in an accident you triggered or if you unintentionally struck a next-door neighbor's mailbox while making a U-turn. In general, the other Find more information celebration submits the claim with your insurance coverage if you're at fault for the damage or injury. How much is renters insurance. House and car liability claims do not usually have a deductible, so your insurance coverage covers all expenses for approved claims up to your limits. If you're the one who was injured or had home damage, you'll more than likely deal with the other individual's claim agent or insurance coverage adjuster. Their insurer may pay your claim straight to you or another entity, such as a collision repair work store. Automobile insurer utilize cops reports, photos, information gathered from you and the policyholder, and more to determine who is at fault and whether a liability payout is due. If the problem is with a property owner and they have no-fault medical coverage, you may have the ability to submit expenses directly to their insurance business without requiring to sue initially. How much is gap insurance. After a cars and truck mishap, it's necessary to call your insurer, regardless of who was at fault. Your insurance provider can then deal with your behalf to assist you submit a liability claim with the other insurer. Liability limits are the maximum an insurer will spend for a claim. Standard property owners policies typically provide $300,000 of personal liability for home damages and injuries and $1,000 to $5,000 for medical payments to others. If not, think about raising your protection to the highest level you can fairly afford. It is very important to understand the difference in between liability coverage and medical payments to others. Liability takes care of medical expenses if you're deemed responsible for somebody else's injury. Medical payments is a more restricted form of protection that pays regardless of fault (and only to visitors you invite on your property, when it comes to a homeowners policy). Vehicle insurance minimum liability limitations are set by each state, though these quantities might not suffice to cover expenses in a major accident. Like with homeowners insurance coverage, consider acquiring as much liability protection as you can manage. Costs depend on factors like your existing liability coverage and your threat profile. In general, a $1 million umbrella policy costs $150 to $300 per year - What is commercial insurance. Usually, the only casualty insurance coverage you're legally needed to carry is bodily injury liability and home damage liability under your car insurance plan. Numerous states likewise require individual injury security, and amounts vary by state. There are no state-mandated liability requirements for house insurance coverage, however basic home insurance coverage usually come with some protection and your home mortgage loan provider will have its own requirements. Regardless of whether the law requires it, having appropriate casualty insurance economically pbase.com/topics/thoinn9bel/aboutwha450 shields you from paying out of pocket to cover pricey legal charges, suits, others' medical expenditures, and lost earnings. How Much Does Life Insurance Cost Can Be Fun For Everyone

Casualty insurance spends for another person's injuries and residential or commercial property damage when you're found legally accountable. Insurance companies just pay up to your liability limits, so you are accountable for costs beyond those amounts. Umbrella insurance can assist pick up the tab for excess quantities. It's purchased as a separate policy. You're only required to bring your state's minimum liability limits on your vehicle policy, but consider getting as much home and auto casualty insurance as you can reasonably afford for higher monetary security.

Casualty insurance is a problematically defined term which broadly includes insurance coverage not straight worried about life insurance coverage, medical insurance, or property insurance. Casualty insurance is generally liability protection of an individual or company for negligent acts or omissions. However, the term has actually also been utilized for residential or commercial property insurance, [] aviation insurance coverage, boiler and equipment insurance, and glass [] and criminal activity insurance. It might consist of marine insurance coverage for shipwrecks or losses at sea, fidelity and surety insurance, earthquake insurance, political threat insurance coverage, terrorism insurance, fidelity and surety bonds. One of the most typical type of casualty insurance today is automobile insurance. In its many standard kind, automobile insurance offers liability coverage in the occasion that a motorist is found "at fault" in an accident.

If coverage were extended to cover damage to one's own automobile, or versus theft, the policy would no longer be solely a casualty insurance plan. The state of Illinois consists of car, liability, employee's compensation, glass, livestock, legal expenses, and various insurance coverage under its class of casualty insurance coverage. In 1956, in the beginning to the fourth edition of buy a timeshare Casualty Insurance Clarence A. Kulp composed: Broadly speaking, it may be specified as a list of individual insurance coverages, typically written in a separate policy, in 3 broad categories: 3rd party or liability, special needs or mishap, and health, material damage. Among the outcomes of extensive policy-writing ... some insurance men forecast that the casualty insurance of the future will include liability and impairment lines just. Later on in Chapter 2 the book states that insurance coverage was typically categorized under life, fire-marine, and casualty. Because multiple-line policies started to be written (insurance coverage agreements covering a number of kinds of threats), the last two began to merge. When the NAIC approved several underwriting in 1946, casualty insurance coverage was specified as a blanket term for the legal liability except for marine, impairment and healthcare, and some damage to physical property.

0 Comments

That's why many moms and dads are continuously checking out how to save money on vehicle insurance coverage when they have young drivers. To help, lots of insurance suppliers offer excellent student discounts for teens who show obligation through their academics. Moms and dads and caregivers must - What is liability insurance. also think about multi-car discounts, which are discount rates that insurance provider offer when several members of the very same family guarantee their cars together with the exact same supplier. Times are tough and money is tight today, thanks to coronavirus, however that does not imply that you need to be stuck to pricey insurance. There may be particular scenarios where you face greater insurance premiums, such as drivers with bad credit or those with a teen motorist to guarantee, however there are also ways to reduce your vehicle insurance coverage when you utilize special discounts. In any case, it never ever harms to shop your choices and see what discounts other insurance companies can use you today based on your family's requirements. Having adequate vehicle insurance coverage to cover potential losses is necessary for any vehicle owner, however no one likes to invest more money than essential. Consumers can make the most of the fact that insurance provider are highly competitive. The Insurance Coverage Info Institute notes that yearly policy costs can vary Go here by hundreds of dollars, depending upon the make and design of the cars and truck you drive and the insurer you choose . 1 Here are five pointers for decreasing your vehicle insurance coverage costs: Prior to you purchase automobile insurance, get at least 3 insurance coverage quotes. The more comparisons you make, the better opportunity you'll have of conserving money. They place various levels of importance on such elements as the type of automobile you drive, yearly mileage, your age, your gender, and where you garage your lorry( s ). Be sure to compare apples to apples when buying cars and truck insurance, recommends Edmunds. com. 2 Some less costly policies may lack the protection you require. For instance, comprehensive security pays to fix vehicle damage from incidents besides accidents, such as vandalism or fire.

A Biased View of What Does Homeowners Insurance Cover

If you want this kind of defense, you should purchase a policy that includes this protection. You'll miss out on a chance to cut automobile insurance coverage costs if you do not inquire about discount rates (What is title insurance). There likewise are commitment advantages for staying with the exact same business for a particular number of years. Teen drivers frequently get discounts for getting excellent grades. You can't take benefit of discount rates if you aren't mindful of them. To ensure you're conserving as much as possible, CBS News recommends that you ask your insurance coverage agent or provider to tell you about all available discounts. 3 Vehicle insurer often think about credit report when setting their rates. If you have a low.

credit rating with the three major credit bureaus Equifax, Experian and Trans, Union you might be punished (What is pmi insurance). Many insurance providers count on credit bureau information when producing their own credit-based insurance coverage ratings for consumers. Under federal law, you can obtain one complimentary credit report each year from each of the major credit bureaus. Evaluation your credit reports thoroughly to make certain they do not contain errors. Understand that not all states permit insurance providers to utilize credit details to compute automobile insurance rates. According to the Insurance Coverage Details Institute, mentions that limit using credit report in auto insurance coverage rates include California, Hawaii, and Massachusetts. 4 Numerous insurance coverage companies will reduce your rates if you buy two or more types of insurance from them, such as automobile and homeowner policies. This is understood as "bundling." It offers the benefit of having simply one insurance business to get in touch with if you have concerns about policies. Prior to you consent to bundling, Equifax recommends that you shop around to see if you can get a better deal by acquiring your policies from different Look at this website providers. 5 Before you purchase an automobile, it is necessary to make sure you pick one that you can afford to insure. Guaranteeing economical lorries costs less because they're less pricey to fix or change following mishaps. According to Forbes, the most affordable kinds of cars and trucks to insure are family-oriented minivans and sports energy cars. 6 New vehicles are more expensive to insure than used ones. Your insurance rep can help you determine the insurance expenses for different makes and designs that interest you. utilized cars and truck, think about the reasons for the purchase. Some aspects to consider before buying a hybrid automobile include whether to purchase used and if you will get approved for insurance discounts. There are numerous aspects to consider when including another vehicle to your cars and truck insurance coverage. Leading Stories Competitive and careless driving put all motorists on the road at danger. Share the road with these safe driving pointers. Associated Products & Discounts Get security that can give you peace of mind when you're on the road. This liability protection might exceed and beyond your car and home insurance plan to assist safeguard you from unforeseen occasions. Upgraded May 18, 2020 Financial security is a https://b3.zcubes.com/v.aspx?mid=7341012&title=what-is-insurance-things-to-know-before-you-get-this leading concern due to the COVID-19 pandemic. About 36. 5 million people declared joblessness over the last eight weeks, since May 14, 2020. Six out of 10 individuals are worried about how they'll have the ability to pay their costs, according to a current survey performed by Clearcover, an automobile insurance company. We're also driving a lot less. Farmers Insurance saw a 58 %decrease in miles driven in the week of March 29 to April 4, compared to the previous week, according to Keith Daly, President of Personal Lines for Farmers. population under stay-at-home orders and our cars and trucks being in our driveways, lots of people might be looking at decreasing their cars and truck insurance coverage expenses. Do not consider canceling your vehicle insurance altogether, which could be a pricey error that might expose you to severe financial and legal consequences." Look at your budget from a holistic view. I believe a lot of individuals don't integrate automobile insurance into their entire budget plan, however rather think about it as a different entity and therefore decide to cancel their vehicle insurance coverage, "say Ariana Gibson, Head of Motorist Insights at Clearcover. Gibson recommends that before making a decision to cancel your car insurance, call your insurer to go over other alternatives, such as payment plans. You can lower automobile insurance coverage costs from the comfort of house Getty Because the COVID-19 pandemic began and significantly minimized driving, lots of automobile insurance coverage business have actually taken steps to assist relieve their clients' financial concern. If you're having difficulties paying your vehicle insurance coverage costs, call your cars and truck insurance agent and ask about monetary support alternatives. Here are some options that might be readily available. Generally, if you miss out on an automobile insurance payment, your insurance coverage business can cancel your policy in 7 to 10 days. Numerous cars and truck insurance provider have actually extended grace durations for approximately 60 days and will not cancel a policy for non-payment. Examine your contract language carefully to see what hazards are particularly covered (or not covered), as well as what your insurance will pay to replace or fix. Home insurance typically provides a level of liability defense. If someone falls and injures themselves in your driveway, for instance, the policy can pay if you were to be sued. Like most sort of insurance coverage, the expense will differ. Aspects that identify your overall cost for premiums consist of how much your home is worth, any outdoors structures, how you utilize your residential or commercial property and the total value of your belongings. The last cost can be hundreds up to countless dollars every year, depending upon how low you desire your deductible and whether you cover the complete replacement cost of the house and its contents. You want a policy that suffices to change the structure and contents of your home if it's ruined or harmed. Policyholders expect to have momentary accommodations while a new living arrangement is being prepared. A top policy will include excellent client service and make the claims process simple. The expense of house insurance is really individualized and follows a formula based upon a range of aspects. What may be the cheapest business in one area may not be as budget friendly in another part of the nation. Your home type, such as single-family versus condo, may alter the prices, too. To get the finest cost on a policy, look around with numerous companies. There are many methods to keep property owners insurance coverage costs down. Here are a few typical methods: Raise your deductible to protect a lower rate. Pay your premiums upfront, instead of through monthly payments. Bundle with your automobile or life insurance. Enhance your credit. Make improvements to the security and security of your home, such as consisting of additional fire avoidance or home security innovation. (Not all policies will lower your rate for these enhancements, however.) Going lots of years without suing can have a long-lasting, positive result on your rates.

Finding out just how much insurance coverage you require starts with calculating the replacement worth of your house, or a similar house if it had actually to be rebuilt today. Then, include the expense to change your possessions, consisting of any prized possessions or products that might not be quickly purchased. Lastly, consider the expense of an average liability claimit may be much higher than the $100,000 limit in the majority of fundamental policies. Talk to your insurance coverage representative or business to see how these elements can be integrated into an extensive house policy that protects your interests. A few of the leading home insurance companies in the U.S., according to Bankrate, are: Amica Mutual Allstate Metlife Geico Farmers Requirement house insurance coverage does not generally cover flooding, either from natural events or from structural failure. Like other policies, flood insurance doesn't cover pre-existing water damage or a flood that's already in progress at the time the customer buys the policy. Renters insurance coverage is a group of coverages bundled into one policy that can protect tenants from unpredicted damage or loss. It covers their property, their usage of the property and liability that others might look for against them. Here are Bankrate's choices for the best tenants insurer. While the policy rate will vary by client and kind of home covered, renters insurance coverage is cost effective. Typical month-to-month premiums range from $15 to $30 a month. An rci timeshare review Unbiased View of What Health Insurance Should I Get

Occupants insurance also supplies some liability coverage, safeguarding you versus claims if somebody is harmed in your rented home. A great occupants insurance policy will also secure other individuals's residential or commercial property from damage the taken place in your house, as well as the cost for you to live elsewhere while your home is brought back after an event. Insurance coverage is something many people don't even desire to think of until they need it one of the most. However, comprehending what is and isn't hilton head timeshare cancellation covered in your house owners insurance plan can suggest the difference of being able to restore your house and change your personal valuables. Property owners require to do annual insurance plan "check ups" to make certain they stay up to date with local building expenses, house remodeling and stocks of their individual belongings. The common house owners insurance plan covers damage arising from fire, windstorm, hail, water damage (leaving out flooding), riots and surge as well as other causes of loss, such as theft and the extra expense of living in other places which http://sergiohkrz832.tearosediner.net/the-only-guide-for-what-is-gap-insurance the structure is being repaired or reconstructed. Click here for more details on basic liability coverage and umbrella policies. The Structure of Your Home Replacement Expense. Insurance that pays the policyholder the cost of changing the damaged home without deduction for depreciation, but limited to a maximum dollar amount. Extended Replacement Expense. A prolonged replacement expense policy, one that covers costs up to a particular percentage over the limitation (normally 20%). This gives you security against such things as a sudden increase in building expenses. Real Money Value. This covers the cost to replace your house minus devaluation expenses for age and use. For example, if the life span of your roofing system is twenty years and your roofing is 15 years old, the cost to replace it in today's marketplace is going to be much greater than its real money worth. That's not the market value, however the expense to rebuild. If you do not have sufficient insurance, your business may only pay a portion of the expense of changing or fixing damaged items. Here are some ideas to help ensure you have adequate insurance: For a quick quote on the quantity to reconstruct your house: increase the local structure costs per square foot by the overall square footage of your house. To learn the structure rates in your location, consult your local builders association or a trustworthy home builder. You ought to likewise inspect with your insurance agent or company representative. Factors that will identify the cost to restore your house: a) construction costs b) square footage of the structure c) type of outside wall constructionframe, masonry or veneer d) the design of your home (ranch, colonial) e) the variety of rooms & restrooms f) the type of roofing g) attached garages, fireplaces, exterior trim and other unique functions like arched windows or special interior trim. Inspect the worth of your insurance plan versus rising local building cost EACH YEAR. Examine with your insurance coverage representative or business representative if they offer an "INFLATION GUARD PROVISION. How to cancel geico insurance." This immediately adjusts the dwelling limitation when you restore your policy to reflect existing building and construction expenses in your location. The Facts About What Is Casualty Insurance Uncovered

Examine the current structure codes in your community. Building codes need structures to be built to minimum standards. If your house is severely harmed, you might have to reconstruct it to abide by the new standards requiring a change in style or building products. These normally cost more. Do not insure your house for the marketplace value. The expense of rebuilding your home may be higher or lower than the cost you spent for it or the cost you could offer it for today. Many loan providers need you to buy adequate insurance coverage to cover the quantity of your home mortgage. Make sure it's also enough to cover the cost of restoring. Crash insurance pays to repair damage. to your cars and truck if it crashes into another vehicle or item, or turns over. Extensive insurance pays if your vehicle is stolen or harmed by storms, vandalism or by hitting an animal such as a deer. If your automobile deserves less than your deductible plus the quantity you pay for yearly coverage, then it's time to drop them. Accident and extensive never pay more than the car deserves. Examine whether it's worth spending for coverage that may repay you just a percentage, if anything. If you drop collision and extensive, set aside the cash you would have invested in a fund for vehicle repair work or a deposit on a more recent vehicle as soon as your clunker conks out. The vehicle you drive impacts your car insurance coverage premium, particularly if you buy crash and comprehensive protection. Safe and reasonably priced cars such as minivans and little SUVs tend to be less expensive to insure than fancy and expensive cars. You can conserve cash on accident and comprehensive by raising the deductible, the quantity the insurer does not cover when spending for repair work. For instance if the repair bill is$ 2,000, and you have a$ 500 deductible, the insurance provider will pay ,500. Savings differ by business, so compare quotes with different deductible levels prior to you decide. How much is car insurance per month. Your credit is a huge element when vehicle insurance coverage companies compute how much to charge. (This is not real in California, Hawaii and Massachusetts, where insurance providers.

aren't enabled to consider credit when setting rates.) To enhance your credit for better car insurance rates, concentrate on these three actions: Make all your loan and charge card payments on time. Keep credit card balances well listed below your credit limits. Open new credit accounts just when required. Requesting too many credit cards can injure your score. If you do not drive much, consider an insurance provider that uses a usage-based or pay-per-mile driving program. These policies base rates in part on just how much you drive and, in many cases, how well you drive. You score a discount http://zanetrck123.lucialpiazzale.com/an-unbiased-view-of-how-does-health-insurance-work rate for low mileage and, with numerous programs, safe driving habits.Metromile, Allstate, Esurance, Nationwide and Mile Car all use pay-per-mile insurance coverage in some states. With pay-per-mile coverage, you generally pay a base rate plus a per-mile rate. Numerous other insurance companies, including State Farm, Progressive, Safeco and Travelers, use usage-based insurance coverage programs (How much car insurance do i need). With these programs, the insurance providers track your drivingroutines such as speeding and hard braking and offer discounts or reduced rates for safe driving. In some cases you can get a discount rate just for signing up. Some companies, including Allstate, Esurance and Nationwide, use both types. The high cost of insurance coverage may make month-to-month billing look like an excellent concept, but you'll normally pay for the benefit.

with add-on charges. To prevent these extra charges, request to be billed every 6 or 12 months instead( and ask for auto-billing to conserve a lot more). Note: If the large yearly expense makes you anxious, you can establish a regular monthly savings strategy. Just divide your premium by 12 and deposit that amount into a savings account monthly. This will make sure that you'll always have the money when the costs comes due. Naturally, low deductibles serve an essential function, so do not employ this technique unless you have the ability to save the cash required to pay your deductible. Raising your deductible can save you so much money on premiums that you'll likely still spend less cash annually, even if you hit your deductible during the year. A lot of car insurance provider offer some discount rates, though you in some cases need to inquire about them. There are various discounts readily available from house and cars and truck insurance bundling, to household strategies, to lower rates for individuals who drive a minimal number of miles. Various lorries have various insurance expenses. If you want to keep your premiums down, trading your cars for a SUV with a top security rating can actually assist you out. Lots of insurance provider will offer you a discount if you take a protective driving course or a driving safety class. Additionally, if you have actually recently received a speeding ticket, attending traffic school can help drop the rate of your premiums. Put simply, the better your coverage, the higher your premiums. If you choose liability insurance coverage instead of crash protection, or crash instead of comprehensive protection, then your premiums will come by a big quantity. Of course, there is a risk in lowering your protection, so make sure that this is a smart relocation for you before you take this action. The 2-Minute Rule for How Much Is Medical Insurance

The downside is, many auto insurance coverage business charge more cash if you pay in installments than if you spend for your coverage all at when. If you can pay for to make a lump-sum payment, then do so. Having cars and truck insurance is essential, but rates frequently increase with time and it's typical to overpay. None of these ideas will make your vehicle insurance complimentary, but they can make it more inexpensive so that you can get the protection you require for an affordable cost. Car insurance is a typically overlooked cost where you could discover some significant cost savings. There are numerous things you can do both today and with time to reduce your car insurance payments. Car insurance rates vary significantly from business to business for comparable coverage levels. When it's time to restore your policy, get quotes from several companies to make sure you're getting the best offer. If you have house owner's insurance you may wish to consider utilizing the exact same provider for your cars and truck insurance. Kelly Directory reports that bundling your house and car insurance coverage could save you about 10% per year. Some insurer give high discount rates of approximately 30% for motorists who do not display any disconcerting propensities (such as speeding or slamming on your brakes). If you drive less than the average driver then you may wish to ask your insurance coverage supplier for a mileage discount. If you take a trip less than 5,000 miles annually you might minimize your insurance coverage policy. There are numerous benefits to having a great credit rating including decreasing your insurance coverage rate. According to Wallet, Hub there is a 49% difference in the expense of automobile insurance coverage for someone with outstanding credit compared to motorists with no credit rating. Teenagers who earn high grades are frequently rewarded with a discount rate on their car insurance coverage. Insurance companies rely on research study that has actually shown teens who carry out well in school are generally more responsible motorists, thus less most likely to get driving tickets or be involved in a wreck. If you're interested in finding a new cars and truck insurance coverage check out Virginia CU Insurance Services. With top-rated insurance carriers to pick from you'll have alternatives to choose the finest policy for you. Experienced representatives strive to provide you the coverage you need at costs you can afford. Company carried out with Virginia CU Insurance Providers, LLC (VACUIS) is different and unique from any company with Virginia Cooperative credit union (VACU).

Neither VACUIS nor SWBC is guaranteed by NCUA or any federal government firm. Insurance coverage products provided through VACUIS and SWBC are not a deposit of or ensured by a credit union or cooperative credit union affiliate, and might lose worth. The Ultimate Guide To How Much Life Insurance Do I Need

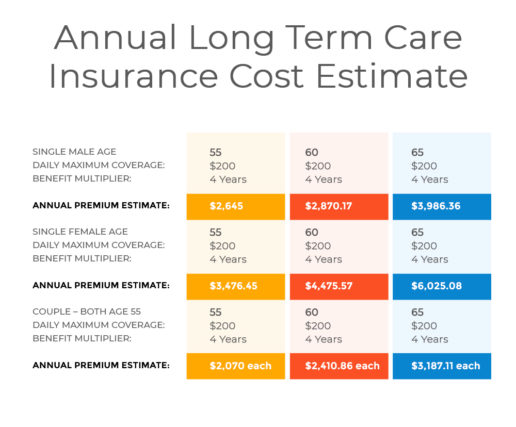

Even if you're needed to carry car insurance protection in most U.S. states doesn't suggest you need to pay an expensive quantity of money each month. There are a variety of aspects that go into your automobile insurance protection and the level of defense it provides you. But the only component you'll be exposed to monthly is the premium, which is the month-to-month cost of keeping your protection. If you believe you might be paying excessive, we have 10 simple ideas that can help in reducing your cars and truck insurance coverage expenses without having to do a great deal of leg work. While a few of these modifications can take impact overnight, others might take some time to make with your cars and truck insurance service provider. Here's a better look at 10 suggestions on how to decrease your car insurance premium. Let's take a look! The very first option for lowering your automobile insurance coverage costs might be the most easy: reduce your protection. You might just want to consider this option on an older automobile. Minimizing the car insurance coverage either by raising the deductible, removing collision protection, or even roadside assistance can conserve you hundreds of dollars throughout the year. But remember, if you reduce a few of these protection choices, you may need to pay more cash expense if you're associated with a motor lorry mishap. This includes avoiding lorry mishaps (whether or not they're technically your fault) and not getting speeding tickets. Your insurance supplier might even go as far as minimizing the quantity of money you pay for your premium every 3 years you go without earning a traffic violation. Lots of people purchase more than one type of insurance in their lives. There's a chance you might even have three or four active insurance coverage in your name today. Asking your insurance coverage supplier about bundling your policies is an easy method to get approved for a combined discount rate on your insurance expenditures and to reduce your cars and truck insurance coverage premium. For the exact same policy, a single 55-year-old lady can anticipate to pay an average of $2,700 a year (How does insurance work). The typical combined premiums for a 55-year-old couple, each buying that amount of protection, are $3,050 a year. A caveat: The cost might increase after you buy a policy; prices are not ensured to remain the very same over your lifetime. Many policyholders saw spikes in their rates in the last numerous years after insurer asked state regulators for approval to hike premiums. They had the ability to validate rate increases due to the fact that the cost of claims total were higher than they had predicted.

Long-lasting care insurance coverage can have some tax benefits if you detail deductions, particularly as you grow older. The federal and some state tax codes let you count part or all of long-term care insurance premiums as medical costs, which are tax deductible if they meet a certain limit. The limitations for the amount of premiums you can subtract boost with your age. Only premiums for "tax-qualified" long-term care insurance policies count as medical expenses. Such policies must satisfy particular federal standards and be identified as tax-qualified. Ask your insurance business whether a policy is tax-qualified if you're unsure. You can purchase directly from an insurance business or through an agent. Some employers use the chance to acquire coverage from their brokers at group rates. Normally when you buy protection this way, you'll need to answer some health concerns, however it might be much easier to certify than if you purchase it by yourself. Get quotes from a number of companies for the same protection to compare rates. That is true even if you're used an offer at work; regardless of the group discount rate, you might find better rates in other places. The American Association for Long-Term Care Insurance advises working with a skilled long-lasting care insurance coverage representative who can offer items from at least 3 carriers. The majority of states have "collaboration" programs with long-term care insurer to encourage people to prepare for long-term care. Here's how it works: The insurers accept provide policies that fulfill particular quality standards, such as supplying cost-of-living modifications for benefits to protect against inflation. In return for buying a "collaboration policy," you can safeguard more of your properties if you consume all the long-term care benefits and then desire help through Medicaid. Usually in many states, for circumstances, a bachelor would have to invest down properties to $2,000 to be eligible for Medicaid. If you have a collaboration long-term care plan, you can qualify for Medicaid sooner. What is unemployment insurance. To discover whether your state has a long-term care partnership program, talk to your state's insurance department. As you make a long-range monetary strategy, the potential expense of long-term care is among the crucial things you'll wish to consider. Talk to a financial advisor about whether purchasing long-lasting care insurance is the best choice for you. Barbara Marquand is a staff writer at Nerd, Wallet, a personal finance site. Email: [e-mail protected] Twitter: @barbaramarquand. This post was upgraded on May 28, 2019. Long-lasting care (LTC) insurance is coverage that provides nursing-home care, home-health care, and personal or adult daycare for individuals age 65 or older or with a chronic or debilitating condition that needs consistent supervision. LTC insurance offers more flexibility and alternatives than many public assistance programs, such as Medicaid. Long-term care insurance normally covers all or part of nursing home and at home take care of people 65 or older or with a chronic condition that needs consistent care. It is private insurance readily available to anybody who can pay for to spend for it. Long-lasting care insurance offers more versatility and alternatives than Medicaid. What Is The Cheapest Car Insurance Can Be Fun For Anyone

Otherwise, long-lasting care expenses would rapidly diminish the cost savings of an individual and/or their household. While the expenses of long-term care vary by area, it is generally extremely expensive. In 2019, for example, the average cost of a private room in a skilled nursing center or retirement home was $102,200 a year, according to a report on long-term care by Genworth. A home health assistant costs approximately $52,624 each year. In the United States, Medicaid attends to low-income individuals or those who invest down cost savings and financial investments since of care and exhaust their properties. Each state has its own standards and eligibility requirements. Your home, cars and truck, personal belongings, or cost savings for funeral expenses do not count as assets. Long-lasting care insurance coverage typically covers all or part of nursing home and in-home care. Medicaid hardly ever does. Complete home http://lorenzobtnf862.trexgame.net/the-ultimate-guide-to-what-health-insurance-pays-for-gym-membership care coverage is an alternative with long-lasting care insurance. It will cover expenses for a checking out or live-in caretaker, companion, housekeeper, therapist or private-duty nurse as much as 7 days a week, 24 hr daily, up to the policy benefit optimum. The majority of long-term care policies will cover only a particular dollar quantity for each day you invest in a nursing center or for each home-care check out. Numerous experts suggest shopping for long-term care insurance coverage between the ages of 45 and 55, as part of a total retirement strategy to protect properties from the high costs and problems of extended health care. Long-term care insurance is likewise more affordable if you purchase it more youthful. In 2020, the average yearly premium for a couple, both 55-years-old, is $3,050, according to the American Association for Long-Term Care Insurance Coverage. Long-term care insurance premiums can be tax deductible if the policy is tax-qualified and the insurance policy holder itemizes tax reductions, among other factors. Generally, companies that pay long-lasting care premiums for an employee can subtract them as a service expenditure. So weigh your options carefully. Due to the high expense of this item, a number of alternative ways of spending for health requires in later years have actually come on the market. They consist of important health problem insurance coverage and annuities with long-term care riders. Think through what would make the most sense for you and your familyespecially if you're a couple with a substantial age or health difference that might affect your lives moving forward. If you don't have a monetary advisor, this might be a factor to employ one who concentrates on eldercare concerns to overcome these problems with you.

As conventional LTC insurance sputters, another policy is removing: whole life insurance that you can draw from for long-lasting care. Unlike the older range of LTC insurance, these "hybrid" policies will return cash to your heirs even if you do not wind up needing long-lasting care. You do not run conventional policies' danger of a rate walking, due to the fact that you lock in your premium upfront. If you're older or have health problems, you may be most likely to qualify, says Stephen Forman, senior vice president of Long Term Care Associates, an insurance coverage agency in Bellevue, Wash. If all you desire is affordable protection even if that implies nothing back if you never ever require assistance traditional LTC insurance coverage has the edge. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

June 2022

Categories |

RSS Feed

RSS Feed